Going solar doesn’t have to strain your finances. With today’s flexible payment options and significant tax incentives, installing solar panels has become more accessible than ever before. Most homeowners can now choose from multiple financing paths, including solar loans with rates as low as 2.99%, zero-down leasing arrangements, and power purchase agreements (PPAs) that require no upfront investment.

The federal solar tax credit currently offers a 30% reduction in your solar system’s total cost, while state and local incentives can push total savings up to 50% of the installation price. Combined with monthly energy bill savings averaging $100-$200, most homeowners see their solar investment pay for itself within 5-8 years.

Whether you’re looking to reduce your carbon footprint, protect against rising energy costs, or increase your home’s value, modern solar financing makes it possible to start benefiting from clean energy while keeping your initial costs manageable. From traditional home equity loans to specialized solar financing programs, there’s a payment solution to match nearly every budget and financial situation.

Let’s explore your options for making the switch to solar power both affordable and financially rewarding.

Solar Financing Options That Work for Your Budget

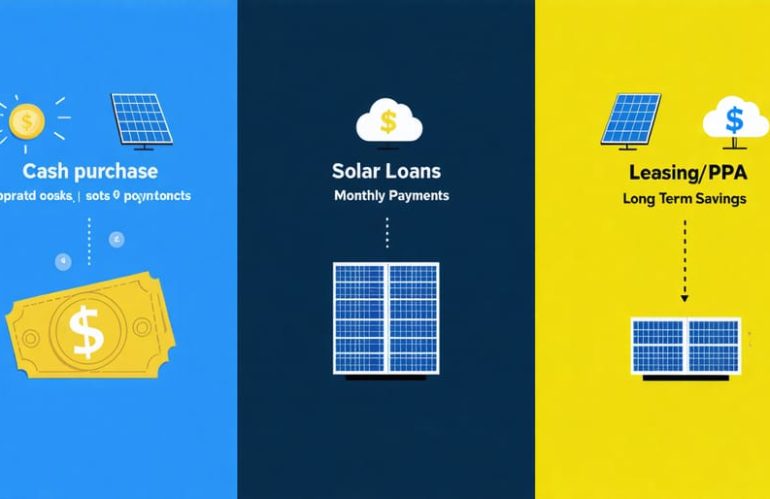

Cash Purchase: Maximum Long-term Savings

Paying cash for your solar system offers the highest potential for long-term savings by eliminating interest payments and financing fees. While the upfront cost may be substantial, typically ranging from $15,000 to $25,000, this approach provides immediate ownership and full access to tax incentives and rebates. Unlike financing options, cash purchases allow you to start saving on energy bills right away without monthly loan payments. If you’re considering installing solar panels yourself, a cash purchase gives you more flexibility in choosing your installation method. Additionally, homeowners who pay cash often see a return on investment in 5-7 years, compared to 7-10 years with financed systems. This option also typically increases home value more significantly since there are no liens or agreements attached to the property.

Solar Loans: Like a Mortgage for Your Energy

Solar loans function similarly to a home mortgage but are specifically designed for financing your solar installation. These loans typically come in two main varieties: secured and unsecured. Secured solar loans use your home as collateral and often offer lower interest rates, while unsecured loans don’t require collateral but may have slightly higher rates.

Many solar installers partner with lending institutions to offer in-house financing options, making the process seamless. These loans usually range from 5 to 20 years, with interest rates typically between 3% and 8%, depending on your credit score and the loan terms.

One popular option is the FHA PowerSaver loan, which allows homeowners to borrow up to $25,000 for solar installations and other energy improvements. Local credit unions and banks also offer specialized green energy loans with competitive rates.

The benefit of solar loans is that your monthly loan payment is often less than your current electricity bill, creating immediate positive cash flow. Plus, you’ll own the system outright once the loan is paid off, maximizing your long-term savings and home value.

Solar Leases and PPAs: No Money Down Options

Solar leases and Power Purchase Agreements (PPAs) offer an attractive path to solar adoption without requiring upfront costs. These financing options allow homeowners to “rent” their solar system or purchase the power it produces at rates typically lower than utility prices.

With a solar lease, you pay a fixed monthly amount to use the system, while with a PPA, you pay for the actual power generated at a predetermined rate. Both options include system maintenance, repairs, and monitoring handled by the solar company, eliminating worry about upkeep costs.

The main advantages include immediate energy savings, professional maintenance, and the ability to go solar without depleting savings. However, these options usually provide lower long-term savings compared to purchasing a system outright. Additionally, the solar company, not you, receives any available tax incentives and rebates.

Before signing, carefully review terms regarding rate increases, contract length (typically 20-25 years), and transfer options if you sell your home. While these zero-down options make solar accessible to more homeowners, they’re best suited for those who prioritize immediate savings over maximum long-term returns.

Money-Saving Incentives You Can’t Ignore

Federal Tax Credit: Your Biggest Savings

The federal solar tax credit stands as one of the most significant financial incentives for homeowners going solar. As of 2024, this credit allows you to deduct 30% of your total solar system costs from your federal taxes. This substantial benefit applies to both the equipment and installation costs, making it a game-changer for your solar investment.

For example, if your solar system costs $20,000, you could receive a $6,000 tax credit. Unlike a deduction, a tax credit reduces your tax liability dollar for dollar, potentially resulting in a larger tax refund or lower tax bill. The best part? If you can’t use the entire credit in one year, you can carry the remaining amount forward to future tax years.

To qualify, you must own your solar system (rather than lease it) and install it at your primary or secondary residence in the United States. The 30% credit is guaranteed through 2032, making now an ideal time to invest in solar energy. Remember, while this credit significantly reduces your overall costs, you’ll need to pay for the system upfront and claim the credit when you file your taxes.

Keep in mind that this federal incentive can be combined with state and local rebates, utility incentives, and other programs, maximizing your potential savings even further.

State and Local Incentives

Beyond federal incentives, many states, cities, and local utilities offer additional financial support for solar installations. These location-specific incentives can significantly reduce your overall investment and accelerate your return on investment.

Common state-level incentives include tax credits, rebates, and performance-based incentives that pay you for the energy your system produces. Some states also offer Solar Renewable Energy Certificates (SRECs), which you can sell to utility companies. Before proceeding with your project, be sure to check your local solar installation requirements and available incentives.

Many utility companies provide additional rebates or performance-based incentives. Some municipalities offer property tax exemptions for solar installations, ensuring your property taxes won’t increase despite the added home value. Local governments might also waive permit fees or expedite the approval process for solar projects.

To find available incentives in your area, visit the Database of State Incentives for Renewables & Efficiency (DSIRE) website or consult with local solar installers who can guide you through the application process for these programs.

Utility Company Programs

Many utility companies offer attractive incentives to help homeowners transition to solar power. These programs typically include upfront rebates that can significantly reduce your initial installation costs. Additionally, most utilities provide net metering benefits, allowing you to earn credits for excess energy your system produces and feeds back into the grid.

Check with your local utility provider for specific programs in your area, as offerings vary by location. Some common benefits include performance-based incentives, which pay you for the actual energy your system generates, and solar renewable energy certificates (SRECs) that you can sell for additional income.

To maximize these benefits, schedule a consultation with your utility company before installation. They can explain their specific programs, help you understand eligibility requirements, and ensure your system meets their technical specifications. Many utilities also offer energy efficiency audits and additional incentives when you combine solar installation with other energy-saving improvements.

Remember to factor these utility incentives into your overall financial planning, as they can substantially improve your system’s return on investment.

Making the Smart Financial Choice

Comparing Your Options

Each financing option offers distinct advantages and considerations. Here’s how they stack up:

Cash Purchase

• Highest upfront cost but maximum long-term savings

• No interest payments or monthly fees

• Full ownership and warranty benefits immediately

• Eligible for all tax incentives and rebates

• Typical break-even period: 5-7 years

Solar Loans

• Minimal to no upfront costs

• Monthly payments often lower than current utility bills

• Full ownership benefits and tax incentives

• Interest rates typically between 3-8%

• Break-even period: 7-10 years

Solar Lease/PPA

• Zero to minimal upfront costs

• Predictable monthly payments

• No maintenance responsibilities

• Limited to no tax benefits

• Break-even period: Not applicable (no ownership)

Home Equity Options

• Lower interest rates than most solar loans

• Tax-deductible interest payments

• Longer repayment terms available

• Uses home as collateral

• Break-even period: 6-8 years

Your best choice depends on several factors:

• Available cash for upfront investment

• Credit score and financing eligibility

• Home ownership timeline

• Desired maintenance responsibility

• Tax situation and ability to claim incentives

Consider consulting a financial advisor to determine which option aligns best with your financial goals and circumstances.

Questions to Ask Before You Choose

Before making your final decision on solar financing, consider these crucial questions to ensure you’re making the best choice for your situation. Start by evaluating your long-term plans: How long do you intend to stay in your current home? This affects whether a longer-term loan makes sense for you.

Assess your financial readiness by calculating your current energy costs and comparing them to potential solar savings. What’s your credit score, and how might it impact your financing options? Understanding these factors will help you secure better terms.

Consider the system’s total cost: Have you received multiple quotes from reputable installers? Don’t forget to factor in maintenance costs and potential repairs. Also, research available incentives: Are there local rebates or tax credits you can utilize? Make sure to understand their requirements and deadlines.

Evaluate different financing options: Can you make a significant down payment to reduce monthly costs? Have you compared interest rates from various lenders? You might want to get expert advice on which financing method best suits your circumstances.

Finally, review the warranty terms and understand who’s responsible for maintenance. What happens if you need to sell your home? Having clear answers to these questions will help you make an informed decision about financing your solar installation.

Real Numbers: What Other Homeowners Are Paying

To give you a clear picture of what real homeowners are paying for their solar systems, let’s look at some recent examples from across the country. In California, the Johnson family installed a 6kW system for $18,000 after federal tax credits, financing it through a solar loan with 4.99% APR over 12 years. Their monthly payment is $165, but they’re saving $220 on their electric bill, resulting in immediate positive cash flow.

In Texas, the Martinez household chose a solar lease for their 8kW system. With zero down payment, they pay $130 monthly for their lease while saving approximately $175 on electricity costs. Their agreement includes maintenance and performance guarantees, providing peace of mind with minimal upfront investment.

The Williams family in Florida opted for a PACE financing program for their 7kW system. Their $22,000 system is being paid through their property taxes, with annual payments of $2,400. Their yearly energy savings of $2,800 more than offset this cost.

These examples show that financing choices vary based on local incentives, electricity rates, and personal preferences. To find the best option for your situation, you can connect with solar experts who can analyze your specific circumstances.

Remember that these numbers are examples, and your actual costs will depend on factors like your location, energy usage, and roof configuration. Many homeowners report breaking even on their investment within 5-8 years, with systems continuing to generate free electricity for decades afterward. When comparing quotes, focus on both the immediate monthly impact on your budget and the long-term savings potential.

Making the switch to solar energy has never been more accessible or financially advantageous. With multiple financing options available, from solar loans and leases to power purchase agreements, homeowners can choose the path that best fits their budget and goals. The federal tax credit, state incentives, and local rebates significantly reduce the initial investment, making solar more affordable than ever before.

Remember that while the upfront costs may seem substantial, solar financing solutions allow you to spread these expenses over time while immediately benefiting from reduced energy bills. Many homeowners find that their monthly solar payments are less than their previous utility bills, creating positive cash flow from day one.

By carefully evaluating your energy needs, financial situation, and available incentives, you can develop a solar financing strategy that works for you. Whether you choose to purchase your system outright, opt for a solar loan, or select a lease agreement, the long-term benefits of solar energy are clear: lower utility bills, increased home value, and a smaller carbon footprint.

Don’t let financing concerns prevent you from joining the solar revolution. Contact local solar providers today to explore your options and receive customized quotes. With the right financing plan in place, you can start generating clean, renewable energy and enjoying significant savings for decades to come.